Our posts to this point have centered on utilizing the third largest asset class (real estate) to gain broader diversification to potentially counterbalance the increasing and corrosive impact of inflation on client portfolios. To support this, we highlighted how commercial real estate and multifamily properties have historically outperformed many traditional, inflation-hedging strategies during different inflationary periods.

In this discussion, we provide “the numbers” to better understand why multifamily properties are generally more sensitive—in a good way—to inflation than other property types. To illustrate the advantage of multifamily apartments over other real estate asset classes, we turn to groundbreaking research conducted by Berkadia, a national leader in commercial real estate servicing and financing.

In its recent landmark study, A Better Way to Assess Inflation and Risk in Real Estate (2021), Berkadia examined the inflation sensitivity and risk-adjusted returns of private real estate, listed REITs, and stocks. Their conclusions were striking.

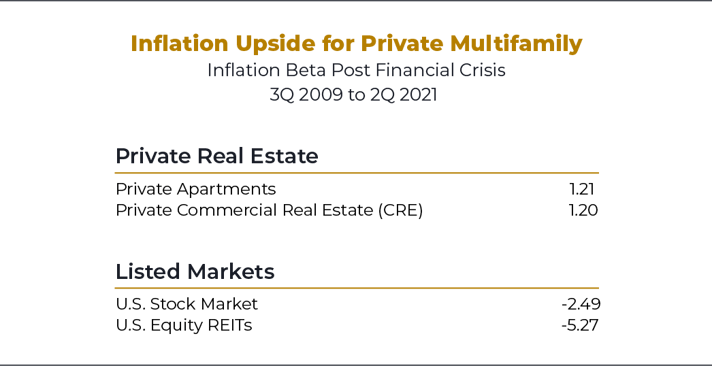

When Inflation Provides Upside

Berkadia illustrated how various types of real estate respond to inflation by calculating “inflation beta.” As investment professionals, we are very familiar with beta as a measure of market sensitivity. For example, an equity index fund may have a market beta of 1, since it is designed to move in tandem with the equity markets. “Inflation beta” shows how sensitive an investment is to inflation.

“Post GFC [Great Financial Crisis], a 1% rise in inflation implies a 1.20% rise in private CRE excess returns. Conversely, over the same period, a 1% rise in inflation implies a decline in the returns of REITs and stocks.”

- Berkadia Research

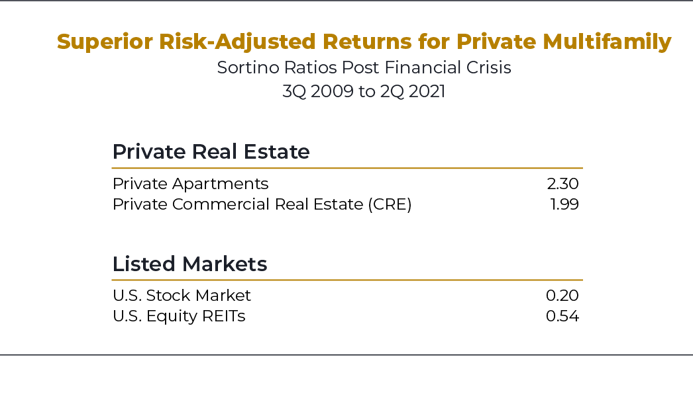

Private Multifamily Risk-Adjusted Returns

Next, Berkadia examined risk-adjusted returns. Berkadia calculated excess return per unit of downside risk using the Sortino Ratio, another highly useful measure of performance, because most investors experience “loss aversion” (losses tend to have higher negative emotional intensity than positive feelings of equal gains). This suggests downside protection is as important—if not more important—to client portfolios.

Thus, the Sortino Ratio can provide a more insightful measure of risk-adjusted returns, calculating excess returns per unit of downside risk.

“U.S. private CRE risk-adjusted returns tend to be larger during times of high inflation.”

“U.S. private CRE risk-adjusted returns tend to be larger during times of high inflation.”

- Berkadia Research

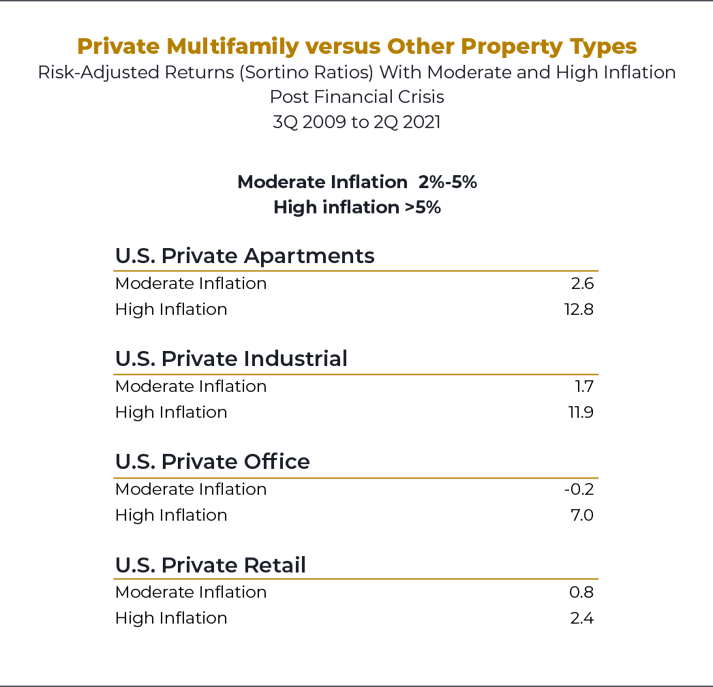

Multifamily Leads Amidst Moderate and High Inflation

Finally, Berkadia examined how different types of private real estate performed against recent inflationary backdrops. Private apartments outperformed on a risk-adjusted basis.

“U.S. private apartments have the strongest risk-adjusted performance during both times of moderate and high inflation.”

- Berkadia Research

Taking Action

Helping to protect your client’s investment portfolios from today’s high and persistent inflation likely means you will need to seriously consider increasing allocations to new investment strategies. Commercial real estate has proven to perform well during inflationary episodes compared to traditional asset classes.

And as Berkadia’s new research reveals, when considering commercial real estate as a potential inflation-hedging asset class, multifamily apartments may be the optimal property type for investing.

If you’d like to learn more about the multifamily investment option, download our FREE eBook, A Potential Inflation Hedge for Today: Private Multifamily Real Estate.

You can also conveniently schedule a one-on-one meeting with me HERE.

Download Our Latest Ebook!

Topics: Insights, Inflation, Multifamily